My own original contribution to the memeosphere.

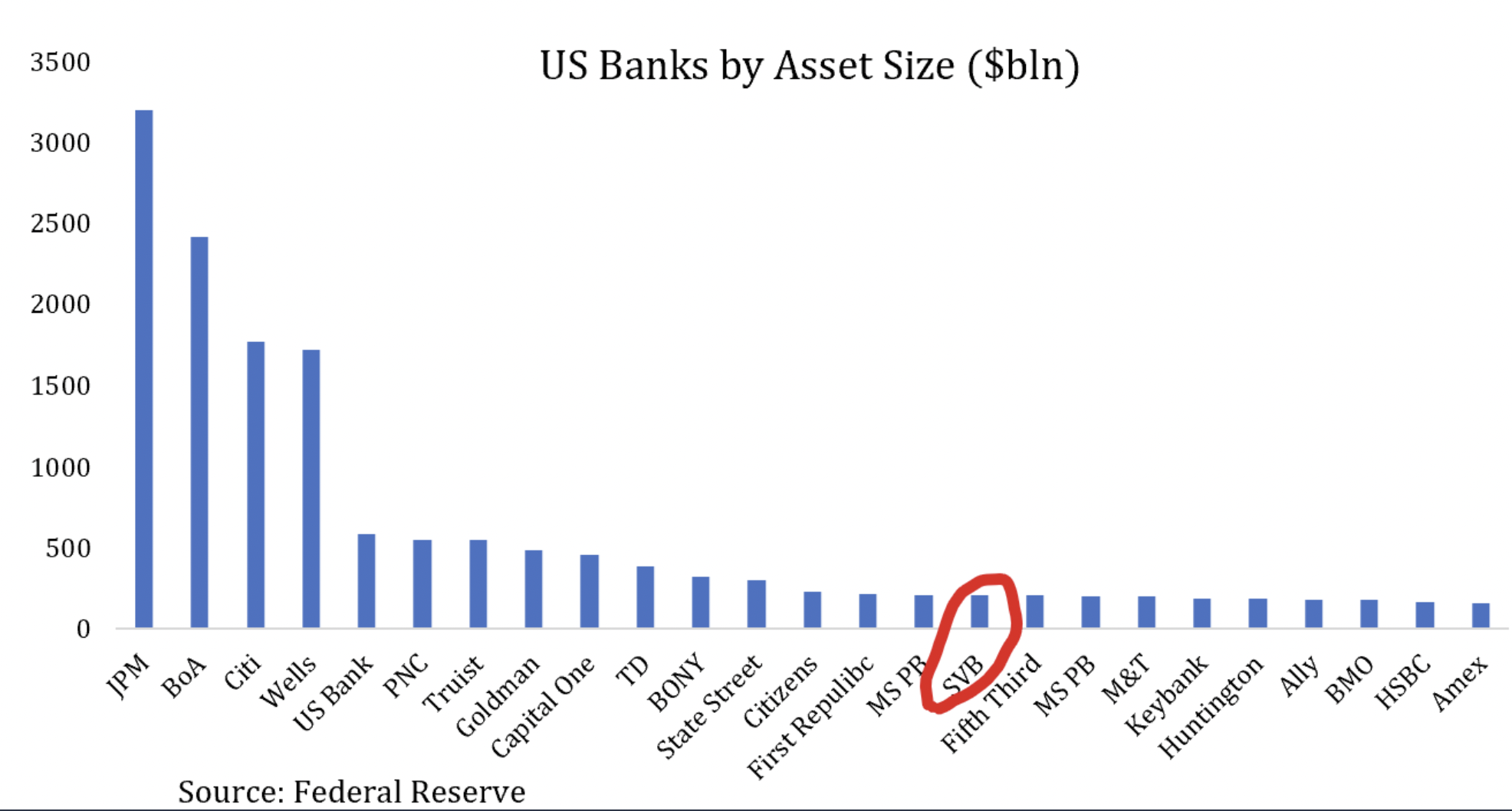

The pixels from my previous post had hardly hit the ether before news broke that the Federal government is going to bail out all Silicon Valley Bank depositors in total, which means Harry and Meghan (apparently large depositors) and all the Silicon Valley start-up companies who had their money in SVB will get it all back. So the billionaire venture capitalists on Sand Hill Road won’t have to re-capitalize their next moon shots themselves. How nice for them. Now get set for the whiplash of Elizabeth Warren and Donald Trump saying more or less the same thing—and they’ll both be right up to a point.

Some observations and questions:

• What is the legal basis for the Federal Reserve, FDIC, and the Treasury to bust the $250,000 lid on deposit insurance? I guess that statutory ceiling was merely optional? A mere suggestion of Congress? Sounds like another “major questions doctrine” test for the Supreme Court—if someone has standing. Could be like the student loan case.

• The statement says:

“No losses associated with the resolution of Silicon Valley Bank will be borne by the taxpayer. . . Any losses to the Deposit Insurance Fund to support uninsured depositors will be recovered by a special assessment on banks, as required by law.”

This is a pure fiction, akin to the “employer’s half” of your Social Security tax, which any decent labor economist will tell you also comes wholly out of your paycheck. The Deposit Insurance Fund is simply an indirect tax on all bank customers.

When the savings and loan crisis engulfed the industry in the late 1980s, Congress had to capitalize the Resolution Trust Corporation at the cost to taxpayers of something like $200 billion—real money at the time—because the government “insurance” fund wasn’t adequate to meet the losses even within the statutory account size limit. If the SVB failure sets up a similar crisis because too many banks have also mismanaged their interest rate risk, we’ll see a sequel, paid for by you and me. (The FDIC shut down Signature Bank in New York Sunday. Hmmm.) Did people really think we could have a decade of near-zero interest rates and not have some banking problems?

• This raises the final question (for now): It is said that our political class is always reacting to the last crisis. How likely is it that Yellen, Biden, et. al., are spooked by a rerun of 2008, and want to get ahead of a systemic collapse of the banking system? Despite all the reassuring “news” of the last decade that our major banks have all passed the periodic “stress test” of the Federal Reserve, fractional reserve banking does remain essentially a confidence game, even with heightened capital requirements. It’s going to be an interesting day on Wall Street tomorrow. (If there’s a crash, I’ll likely be buying. But I always run into burning buildings. . .)

Or maybe there is more to the story. I’ll bet bankers and regulators in Washington haven’t slept much this weekend. What do they know for certain that they aren’t telling us?

A clue, perhaps, from the fed statement:

Finally, the Federal Reserve Board on Sunday announced it will make available additional funding to eligible depository institutions to help assure banks have the ability to meet the needs of all their depositors.

That’s pretty close to what Alan Greenspan said the day after the great crash of October 19, 1987.

For what it’s worth: