As everyone who follows the financial markets knows, the Federal Reserve is trying to walk a fine line, hinting that they’d like to start cutting interest rates, but still worried that inflation is proving too persistent to do it just yet (never mind whether real inflation is actually higher than the official headline rate because of how we measure inflation these days). Further rate hikes seem to be ruled but, though a stray voice from inside the Fed can he heard from time to time saying, not so fast.

The Fed clearly wants to limit market volatility as much as they can. And needless to say, Joe Biden is desperate for interest rate cuts soon to aid his re-election chances.

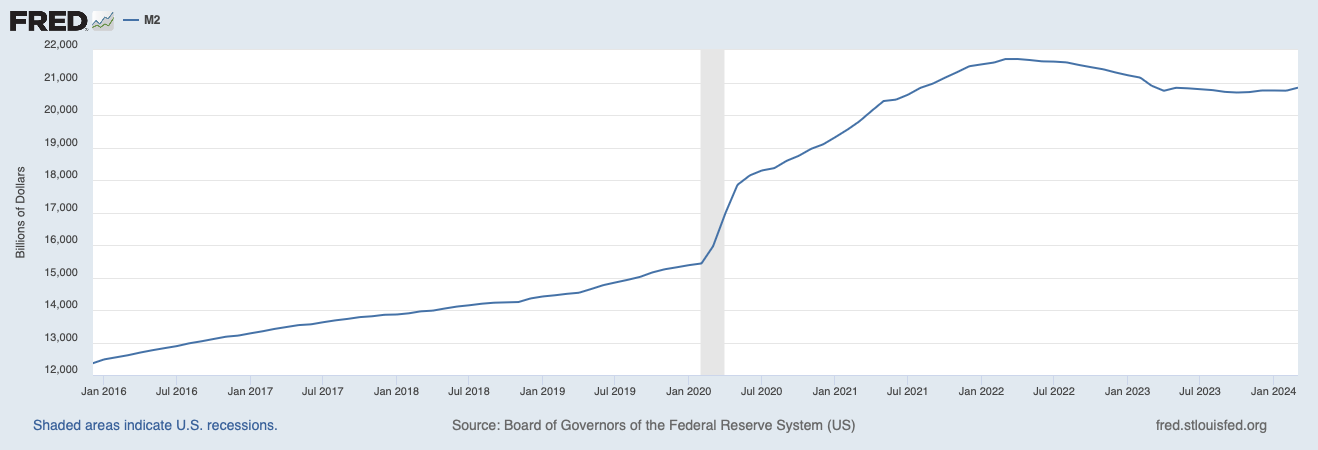

But are interest rates the best or primary tool for reducing inflation? Let’s remember Milton Friedman’s basic rule: inflation is always and everywhere a monetary phenomenon. The most important variable to track is not interest rates, but the money supply, especially the preferred measure, M2. Interest rates can have some effect on M2, but a look at the M2 chart from the St. Louis displays how M2 soared by nearly a third during the Covid over-reaction, and has not come down much since then. Interest rates alone are not necessarily sufficient to bring down the money supply. But they seem to be the best tool for reducing inflationary expectations among consumers, which is an important part of the inflation story.

Jennifer Burns’s new biography of Friedman (full review from me coming shortly) includes this useful reminder:

Friedman had long argued that interest rates were a crude and indirect way of regulating economic activity. He labored to explain that contrary to conventional wisdom, high interest rates did not necessarily mean low inflation or restrained economic growth. Indeed, they could mean the opposite: that inflationary expectations were so entrenched borrowers were willing to take credit at a high price because they thought it would go even higher.

But of course, Joe Biden assured us that “Milton Friedman isn’t running the show any more,” so we can ignore this.